That is the second one put up in a chain of 3, taking into consideration the background to the approaching UK Executive Semiconductor Technique.

Within the first phase, The United Kingdomâs position within the semiconductor global, I mentioned the brand new world setting, through which a tenser geopolitical state of affairs has revived a coverage local weather world wide which is a lot more beneficial to very large scale executive interventions within the business, I sketched the worldwide state of the semiconductor business and attempted to quantify the United Kingdomâs place within the semiconductor global.

Right here, I speak about the previous and long run of semiconductors, citing one of the essential previous interventions via governments world wide that experience formed the present state of affairs, and I speculate on the place the business could be going someday.

After all, within the 3rd phase, Iâll ask the place this leaves the United Kingdom, and speculate on what its semiconductor technique may search to reach.

Energetic commercial coverage within the historical past of semiconductors

The historical past of the worldwide semiconductor business comes to a dance between governments world wide and personal corporations. Against this to the conviction of the predominantly libertarian ideology of Silicon Valley, the business wouldnât have come into life and advanced within the shape we now know with out a collection of main, and dear, interventions via governments the world over.

However, to cool animated film the claims of a few at the left, there may be an concept that it was once governments that created the shopper digital merchandise all of us depend on, and personal business has merely accumulated the income. This view doesnât recognise the large efforts non-public business has made, spending massive sums at the analysis and construction had to very best production processes and produce them to marketplace. Taking the US by myself, in 2022 US the federal government spent $6 billion on semiconductor R&D, in comparison to non-public businessâs $50.2 billion.

The semiconductor business emerged within the Sixties in the US, and in its early days greater than half of of its gross sales have been to the USA executive. This was once an early instance of what we might now name âproject pushedâ innovation, motivated via a âmoonshot ventureâ. The âmoonshot ventureâ of the Sixties was once pushed via an excessively concrete objective â so that you could drop a half-tonne payload any place on this planetâs floor, with a precision measured in loads of meters.

Semiconductors have been necessary to reach this objective â the primary industrially produced computer systems in response to built-in circuits have been advanced because the steerage techniques of Minuteman intercontinental ballistic missiles. After all, in spite of its army driver, this âmoonshotâ produced essential spin-offs â the improvement of house shuttle to the purpose at which a chain of manned missions to the moon have been imaginable, and lengthening civilian packages of the extra a lot less expensive, extra robust and extra dependable computer systems that solid-state electronics made imaginable.

America is the place the semiconductor business began, nevertheless it performed a central function in 3 East Asian construction miracles. The primary to take advantage of this new era was once Japan. Whilst the US was once exploiting the army probabilities of semiconductors, Japan interested in their software in client items.

Via the early 1980âs, regardless that, Eastern corporations have been generating reminiscence chips extra successfully than the US, whilst Nikon took a number one place within the photolithography apparatus used to make built-in circuits. Partially the Eastern aggressive benefit was once pushed via their corporationsâ production prowess and their attentiveness to buyer wishes, however the USA business complained, no longer fully with out justification, that their luck was once constructed at the robbery of highbrow assets, get admission to to unfairly reasonable capital, the safety of house markets via industry obstacles, and executive funded analysis consortia bringing in combination main corporations. Those are ordinary substances of commercial coverage as carried out via East Asian developmental states, first carried out effectively in Taiwan and in Korea, and now being implemented on a continental scale via China.

An an increasing number of paranoid USAâs reaction to this danger from Japan to its technological supremacy in semiconductors was once to undertake some commercial technique measures itself. America comfortable its stringent anti-trust regulations to permit US corporations to collaborate in R&D via a consortium known as SEMATECH, half of funded via the government. Sematech was once based in 1987, and within the first 5 years of its operation was once supported via $500 m of Federal investment, main to a few new self-confidence for the USA semiconductor business.

In the meantime each Korea and Taiwan had known electronics as a key sector wherein to pursue their export-focused construction methods. For Taiwan, a the most important establishment was once the Commercial Era Analysis Institute, in Hsinchu. Since its basis in 1973, ITRI have been instrumental in supporting Taiwanâs commercial base in transferring nearer to the era frontier.

In 1985 the US-based semiconductor government Morris Chang was once persuaded to guide ITRI, the use of this place to create a countrywide semiconductor business, within the procedure spinning out the Taiwan Semiconductor Production Corporate. TSMC was once based as a pure-play foundry, contract production built-in circuits designed via others and specializing in optimising production processes. This way has been greatly a hit, and has led TSMC to its globally main place.

Over the past decade, China has been aggressively selling its personal semiconductor business. The 2015 âMade in China 2025â known semiconductors as a key sector for the improvement of a prime tech production sector, atmosphere the objective of 70% self-sufficiency via 2025, and a dominant place in world markets via 2045.

Reasonable capital for growing semiconductor production was once supplied during the state-backed Nationwide Built-in Circuit Trade Funding Fund, amounting to a few $47 bn (regardless that it kind of feels the report of this fund has been marred via corruption allegations). The 2020 directive âA number of Insurance policies for Selling the High quality Construction of the Built-in Circuit Trade and Instrument Trade within the New Technologyâ bolstered those objectives with a package deal of measures together with tax breaks, comfortable loans, R&D and abilities insurance policies.

Whilst the improvement of the semiconductor business in Taiwan and Korea was once in most cases welcomed via policy-makers within the West, a converting geopolitical local weather has resulted in a lot more nervousness about Chinaâs aspirations. America has spoke back via an competitive programme of bans at the exports of semiconductor production gear, akin to prime finish lithography apparatus, to China, and has persuaded its allies in Japan and the Netherlands to apply go well with.

Commercial coverage in give a boost to of the semiconductor business hasnât been limited to East Asia. In Europe a key part of give a boost to has been the improvement of study institutes bringing in combination consortia of industries and academia; possibly probably the most notable of those is IMEC in Belgium, whilst the cluster of businesses that shaped across the electronics corporate Phillips in Eindhoven now contains the dominant participant in apparatus for excessive UV lithography, AMSL.

In Eire, insurance policies in give a boost to of inward funding, together with each direct and oblique monetary inducements, and the improvement of establishments to give a boost to abilities innovation, persuaded Intel to base their Ecu operations in Eire. This has resulted on this small, previously rural, country changing into the second one biggest exporter of built-in circuits in Europe.

In the United Kingdom, executive give a boost to for the semiconductor business has long gone via 3 phases. Within the postwar duration, the electronics business was once a central a part of the United Kingdomâs Chilly Struggle âWar Stateâ, with executive establishments just like the Royal Alerts and Radar Established order at Malvern sporting out important early analysis in compound semiconductors and optoelectronics.

The second one degree noticed a extra mindful effort to give a boost to the business. Within the mid-to-late 1970âs, a realisation of the possible significance of built-in circuits coincided with a extra interventionist Labour executive. The federal government, during the Nationwide Endeavor Board, took a stake in a start-up making built-in circuits in South Wales, Inmos. The 1979 Conservative executive was once a lot much less interventionist than its predecessor, however two essential interventions have been made within the early 1980âs.

The primary was once the Alvey Programme, a joint executive/non-public sector analysis programme introduced in 1983. This was once an formidable programme of joint business/executive analysis, value £350m, protecting plenty of spaces in knowledge and conversation era. The result of this programme have been blended; it performed a vital function within the construction of cellular telephony, and laid some essential foundations for the improvement of AI and device finding out. In semiconductors, on the other hand, the firms it supported, akin to GEC and Plessey, have been not able to broaden a long-lasting aggressive place in semiconductor production and not live on.

The second one intervention arose from a public schooling marketing campaign ran via the BBC; a small Cambridge founded microcomputer corporate, Acorn, received the contract to provide BBC-branded non-public computer systems in give a boost to of this programme. The huge marketplace created on this manner later gave Acorn the headroom to transport into the workstation marketplace with lowered instruction set computing architectures, from which was once spun-out the microprocessor design home ARM.

Within the 3rd degree, the United Kingdom executive followed a marketplace fundamentalist place. This concerned a withdrawal from executive give a boost to for implemented analysis and the run-down of presidency laboratories like RSRE, and a place of studied indifference in regards to the acquisition of UK era companies via out of the country opponents. Primary UK electronics corporations, akin to GEC and Plessey, collapsed following some ill-judged company misadventures. Inmos was once bought, first to Thorn, then to the Franco- Italian workforce, SGS Thomson. Inmos left a favorable legacy, with many that had labored there happening to take part in a Bristol founded cluster of semiconductor design properties. The Inmos production web site survives as Newport Wafer Fab, lately owned via the Dutch-based, Chinese language owned corporate Nexperia, regardless that its long run is unsure following a UK executive ruling that Nexperia will have to divest its shareholding on nationwide safety grounds.

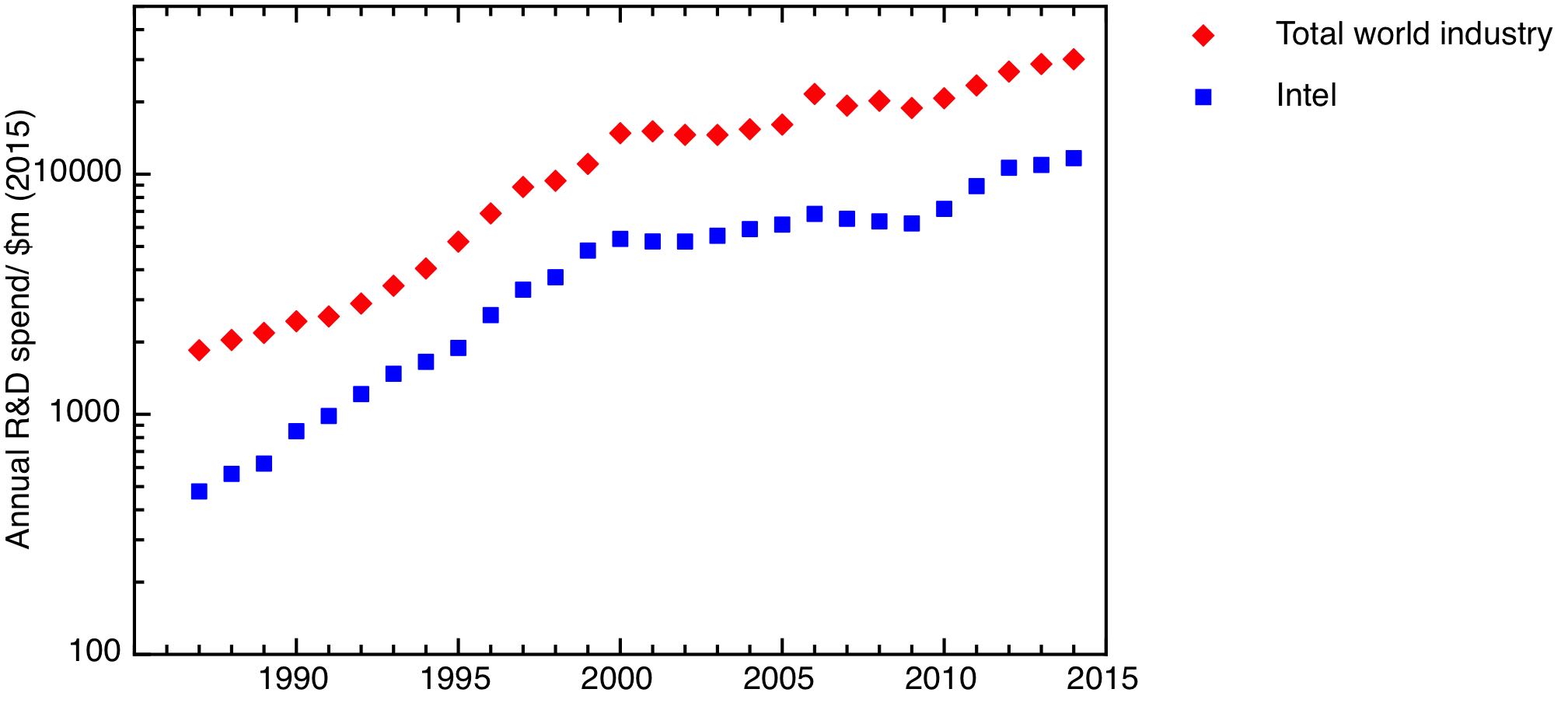

This focal point at the function of interventions via governments the world over at the most important moments within the construction of the business shouldnât overshadow the massive investments in R&D made via non-public corporations world wide. A way of the size of those investments is given via the determine beneath.

R&D expenditure within the microelectronics business, appearing Intelâs R&D expenditure, and a broader estimate of global microelectronics R&D together with semiconductor corporations and kit producers. Information from the âAre Concepts Getting More difficult to In finding?â dataset on Chad Jonesâs web page. Inflation corrected the use of the USA GDP deflator.

The exponential build up in R&D spending as much as 2000 was once pushed via a in a similar way exponential build up in international semiconductor gross sales. On this duration, there was once a outstanding virtuous circle of accelerating gross sales, resulting in expanding R&D, main in flip to very speedy technological trends, riding additional gross sales enlargement. Within the closing 20 years, on the other hand, enlargement in each gross sales and in R&D spending has bogged down

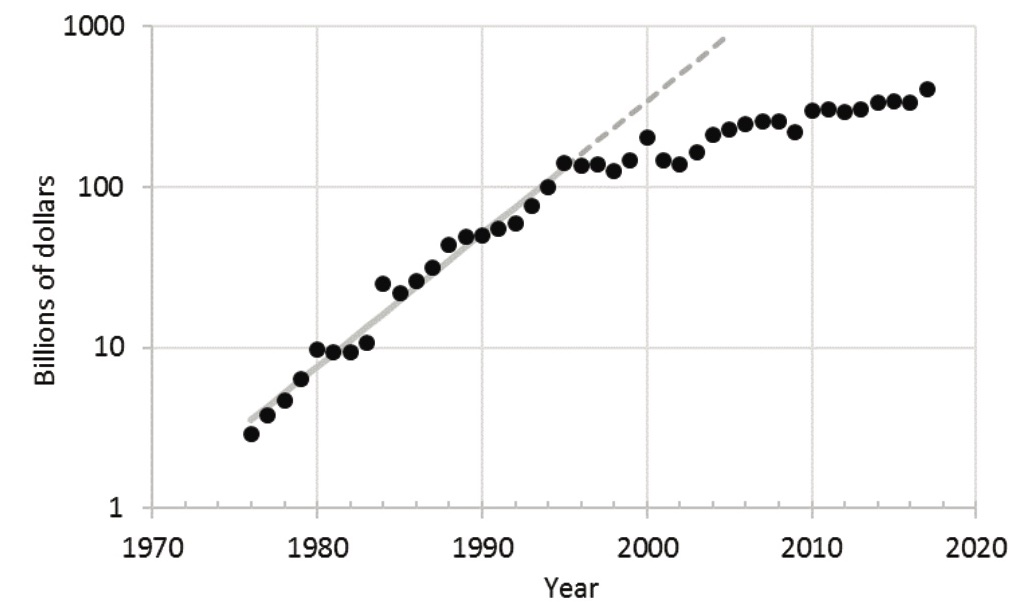

World semiconductor gross sales in billions of greenbacks. Plot from âQuantum Computing: Growth and Potentialitiesâ (2019), Nationwide Academies Press, which makes use of information from the Semiconductor Trade Affiliation.

Conceivable futures for the semiconductor business

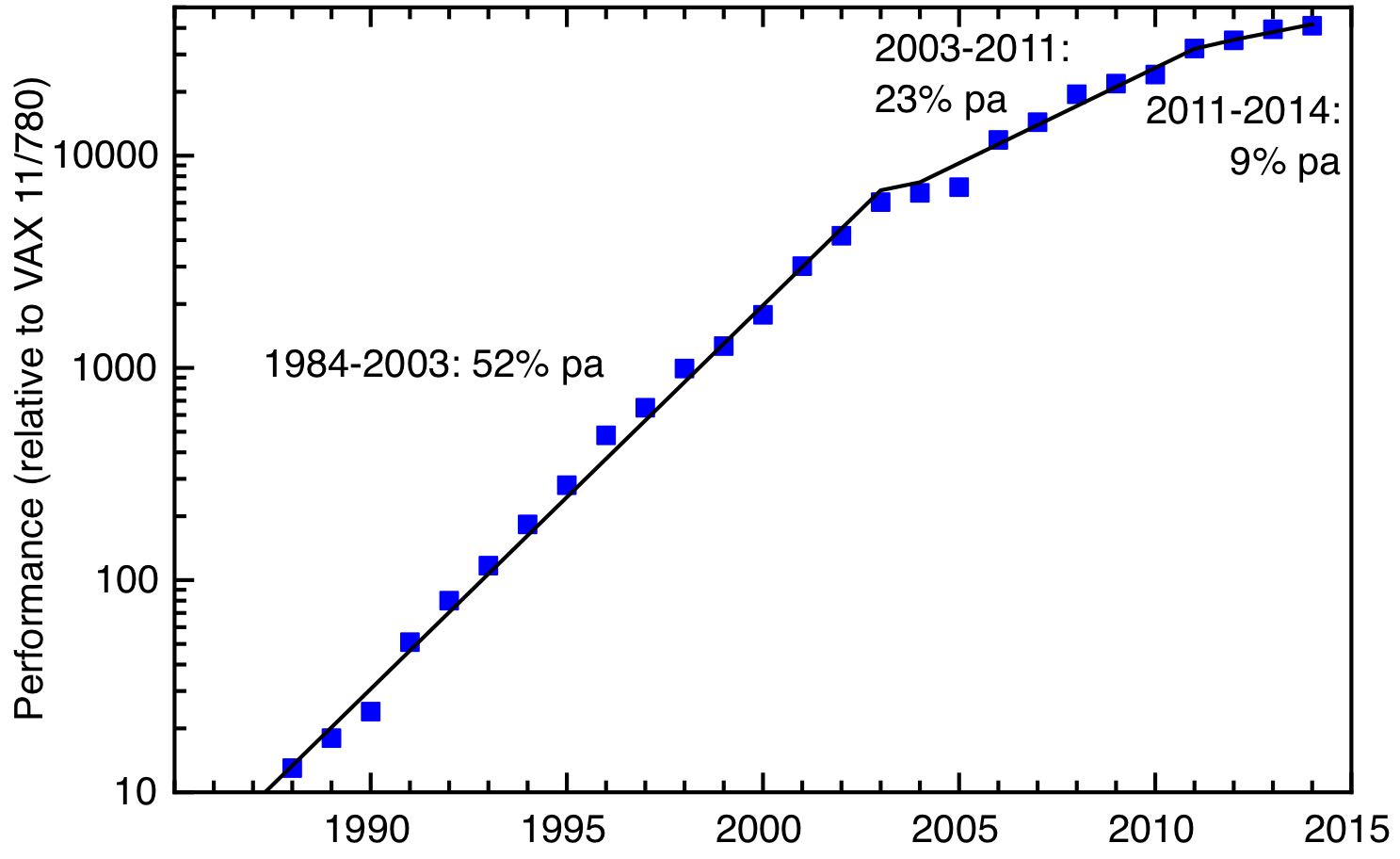

The velocity of technological progrèss in built-in circuits between 1984 and 2003 was once outstanding and extraordinary within the historical past of era. This drove an exponential build up in microprocessor computing energy, which grew via greater than 50% a yr. This enlargement arose from two components, As is well known, the collection of transistors on a silicon chip grew exponentially, as predicted via Mooreâs Legislation. This was once pushed via many unsung, however for my part outstanding, technological inventions in lithography (to call simply a few examples, section shift lithography, and chemically amplified resists), permitting smaller and smaller options to be manufactured.

The second one issue is much less widely recognized â via a phenomenon referred to as Dennard scaling, as transistors get smaller they perform sooner. Dennard scaling reached its restrict round 2004, as the warmth generated via microprocessors changed into a restricting issue. After 2004, microprocessor laptop energy higher at a slower fee, pushed via expanding the collection of cores and parallelising operations, leading to charges of build up round 23% a yr. This way itself bumped into diminishing returns after 2011.

Lately we’re seeing persevered discounts in characteristic sizes, at the side of new transistor designs, akin to finFETs, which in impact permit extra transistors to be fitted right into a given house via construction them side-on. However additional will increase in laptop energy are an increasing number of being pushed via optimising processor architectures for explicit duties, for instance graphical processing devices and specialized chips for AI, and via merely multiplying the collection of microprocessors within the server farms that underlie cloud computing.

Slowing enlargement in laptop energy. The expansion in processor efficiency since 1988. Information from determine 1.1 in Pc Structure: A Quantitative Way (6th edn) via Hennessy & Patterson.

Itâs outstanding that, in spite of the large build up in microprocessor efficiency because the 1970âs, and main inventions in production era, the underlying mode of operation of microprocessors stays the similar. That is identified via the shorthand of CMOS, for Complementary Steel Oxide Semiconductor. Good judgment gates are created from complementary pairs of box impact transistors consisting of a channel in closely doped silicon, whose conductance is modulated via the appliance of an electrical box throughout an insulating oxide layer from a steel gate electrode.

CMOS isnât the one manner of constructing a good judgment gate, and itâs no longer glaring that it’s the highest one. One critical limitation on our computing is its power intake. This issues at a micro degree; the warmth generated via a computer or cell phone could be very glaring, and it was once issues of warmth dissipation that underlay the slowdown within the enlargement in microprocessor energy round 2004. Itâs additionally important at a world degree, the place the power utilized by cloud computing is changing into a vital proportion of general electrical energy intake.

There’s a bodily decrease restrict to the power that computing makes use of â that is the Landauer restrict at the power price of a unmarried logical operation, a result of the second one regulation of thermodynamics. Our present era consumes greater than 3 orders of magnitude extra power than is theoretically imaginable, so there may be room for growth. Someplace within the universe of applied sciences that donât exist, however are bodily imaginable, lies a awesome computing era to CMOS.

Many various types of computing had been attempted out within the laboratory. Some contain other fabrics to silicon: compound semiconductors or new types of carbon like nanotubes and graphene. In some, the bodily embodiment of data is, no longer electrical fee, however spin. The speculation of the use of person molecules as circuit components â molecular electronics â has a protracted and moderately chequered historical past. None of those approaches has but made a vital industrial have an effect on; incumbent applied sciences are all the time arduous to displace. CMOS and its similar applied sciences quantity to a deep nanotechnology applied at a large scale; the massive funding on this era has in impact locked us into a specific era trail.

There are choice, non-semiconductor founded, computing paths which might be value citing, as a result of they are going to transform essential someday. One is to duplicate biology; our personal brains ship monumental computing energy at remarkably low power price, with an structure this is very other from the von Neumann structure that human-built computer systems apply, and a elementary unit this is molecular. Quite a lot of radical approaches to computing take some inspiration from biology, whether or not that’s the new architectures for CMOS that underlie neuromorphic computing, or fully molecular approaches in response to DNA.

Quantum computing, however, provides the potential of some other exponential bounce ahead in computing energy â in concept. Many sensible obstacles stay prior to this doable may also be was practise, on the other hand, and this can be a matter for some other dialogue. Suffice it to mention that, on a timescale of a decade or so, quantum computer systems won’t exchange typical computer systems for anything else greater than some area of interest packages, and after all they’re prone to be deployed in tandem with typical prime efficiency computer systems, as accelerators for explicit duties, reasonably than as common goal computer systems.

After all, I will have to go back to the purpose that semiconductors arenât simply treasured for computing; the sphere of energy electronics is prone to transform increasingly essential as we transfer to a internet 0 power gadget. We will be able to want a a lot more allotted and versatile power grid to house decentralised renewable resources of electrical energy, and this wishes solid-state energy electronics in a position to dealing with very prime voltages and currents â recall to mind changing house-size substations via suitcase-size solid-state transformer. Common uptake of electrical cars and the will for extensively to be had speedy charging infrastructures will position additional calls for on energy electronics. Silicon isn’t appropriate for those packages, which require wide-band hole semiconductors akin to diamond, silicon carbide and different compound semiconductors.

Assets

Chip Struggle: The Battle for the Internationalâs Maximum Crucial Era, via Chris Miller, is a brilliant assessment of the historical past of this era.

Semiconductors in the United Kingdom: On the lookout for a technique. Geoffrey Owen, Coverage Alternate, 2022. Excellent at the historical past of the United Kingdom business.

To Each Factor There’s a Season â classes from the Alvey Programme for Growing an Innovation Ecosystem for Synthetic Intelligence, via Luke Georghiou. Reflections at the Alvey Programme via some of the researchers who performed its reliable analysis.

Are Concepts getting arduous to search out, Bloom, Jones, van Reenan and Webb. American Financial Evaluate (2020). An influential paper on diminishing charges of go back on R&D, taking the semiconductor business as a case find out about.

âQuantum Computing: Growth and Potentialities (2019), Nationwide Academies Press.

Up subsequent: What will have to the United Kingdom do about semiconductors? Phase 3: in opposition to a UK semiconductor technique