JHVEPhoto

Financial Investment Thesis

Dividend payments can be an exceptional source of extra earnings for financiers, especially when the chosen business not just supply Dividend Earnings, however likewise Dividend Development. My financial investment method concentrates on constructing financial investment portfolios that have the goal of supplying you with an appealing mix of Dividend Earnings and Dividend Development, therefore assisting you grow your additional earnings at an appealing rate.

In today’s post that concentrates on high dividend yield business, I will present you to those type of business that can assist you make a considerable quantity of additional earnings in the type of Dividends. Each of these chosen business has strong competitive benefits, is economically healthy, and has an appealing Assessment (8 out of the 10 chosen business have a P/E [FWD] Ratio listed below 10).

These choices might assist you raise the Weighted Average Dividend Yield of your financial investment portfolio and assist you end up being significantly secured from stock exchange cost variations.

Listed below, I will explain the choice procedure in more information. Given that I have actually currently explained this procedure in a previous post, if you are currently acquainted with it you can avoid the following area composed in italics.

Primary step of the Choice Process: Analysis of the Financial Ratios

In order to recognize business with a reasonably high Dividend Yield [FWD], I utilize a filter procedure to make a pre-selection. From this pre-selection, I will later on pick my leading 10 high Dividend Yield business of the month. To be part of this pre-selection of high Dividend Yield stocks, the business must satisfy the list below requirements:

- Market Capitalization > > $10B

- Dividend Yield [FWD] > > 2.5%

- P/E [FWD] Ratio < < 30

In the following, I want to define why I have actually picked the metrics discussed above in order to choose my leading 10 high Dividend Yield stocks of the month.

A Market Capitalization of more than $10B adds to the reality that the threats connected to your financial investments are lower, given that business with a greater Market Capitalization tend to have a lower volatility than business with a low Market Capitalization.

A P/E [FWD] Ratio of less than 30 suggests that the cost you spend for the business is not extremely high, therefore straining those that have stock rates in which high development expectations are priced in. High development expectations suggest strong threats for financiers, given that the stock cost might drop substantially. Once again, the filtering procedure assists us to minimize the danger so that we are most likely to make an exceptional financial investment choice.

2nd action of the choice procedure: Analysis of the Competitive Benefits

In a 2nd action, the business’ competitive benefits (for instance: brand name image, development, innovation, economies of scale, and so on) are evaluated in order to make an even narrower choice. I consider it to be especially essential for business to have strong competitive benefits in order to stand apart versus the competitors in the long term. Business without strong competitive benefits have a greater likelihood of declaring bankruptcy one day, therefore representing a strong danger for financiers to lose their invested cash.

3rd action of the choice procedure: The Assessment of the business

In the 3rd action of the choice procedure, I will dive deeper into the Assessment of the business.

In order to carry out the Assessment procedure, I utilize various approaches and requirements, for instance, the business’ present Assessment as according to my DCF Design, the anticipated substance yearly rate of return as according to my DCF Design and/or a much deeper analysis of the business’ P/E [FWD] Ratio. These metrics must act as an extra filter to just choose business that presently have an appealing Assessment, which assists you to recognize business that are at least relatively valued.

The 4th and last action of the choice procedure: Diversity over Industries and Countries

In the 4th and last action of the choice procedure, I have actually developed the following guidelines for picking my leading choices: in order to assist you diversify your financial investment portfolio, an optimum of 2 business must be from the very same market. In addition to that, there must be at least one choice that is from a business that is based beyond the United States, acting as an extra geographical diversity.

Brand-new Business compared to the previous month of June

- BHP Group Limited ( OTCPK: BHPLF)

- Energy Transfer (NYSE: ET)

- Rio Tinto (NYSE: RIO)

- Société Générale Société anonyme ( OTCPK: SCGLF, OTCPK: SCGLY)

- Swiss RE ( OTCPK: SSREF)

My Leading 10 High Dividend Yield Stocks to Purchase for July 2023

- Altria (NYSE: MO)

- AT&T (NYSE: T)

- BHP Group Limited

- Energy Transfer

- Rio Tinto

- Société Générale

- Swiss RE

- The Bank of Nova Scotia (NYSE: BNS)( BNS: CA)

- United Parcel Service (NYSE: UPS)

- Verizon Communications Inc. (NYSE: VZ)

Summary of the chosen business for July 2023

|

Business Call |

Sector |

Market |

Nation |

Dividend Yield [TTM] |

Dividend Yield [FWD] |

Div Development 5Y |

P/E [FWD] Ratio |

|

Altria Group |

Customer Staples |

Tobacco |

United States |

8.48% |

8.48% |

6.69% |

9.37 |

|

AT&T |

Interaction Solutions |

Integrated Telecommunication Solutions |

United States |

7.01% |

7.01% |

-5.78% |

6.85 |

|

BHP Group |

Products |

Diversified Metals and Mining |

Australia |

8.77% |

5.96% |

24.84% |

13.86 |

|

Energy Transfer |

Energy |

Oil and Gas Storage and Transport |

United States |

8.76% |

9.73% |

-1.43% |

8.95 |

|

Rio Tinto |

Products |

Diversified Metals and Mining |

UK |

7.58% |

6.93% |

10.99% |

7.31 |

|

Société Générale |

Financials |

Diversified Banks |

France |

7.13% |

7.13% |

-6.65% |

6.02 |

|

Swiss RE |

Financials |

Reinsurance |

Switzerland |

6.54% |

6.54% |

4.64% |

3.48 |

|

The Bank of Nova Scotia |

Financials |

Diversified Banks |

Canada |

6.27% |

6.37% |

4.48% |

9.53 |

|

United Parcel Service |

Industrials |

Air Cargo and Logistics |

United States |

3.60% |

3.71% |

12.53% |

16.33 |

|

Verizon Communications |

Interaction Solutions |

Integrated Telecommunication Solutions |

United States |

7.11% |

7.14% |

2.04% |

7.96 |

Source: The Author

BHP Group Limited

BHP Group is a business from the Diversified Metals and Mining Market that was established in 1851 and runs through the following sectors:

BHP Group pays a Dividend Yield [FWD] of 5.96% and it has actually revealed exceptional lead to regards to Dividend Development: the business’s Dividend Development Rate [CAGR] over the previous ten years is 10.05%, which lies 69.77% above the Sector Mean.

This mix in between a reasonably high Dividend Yield and an appealing Dividend Development Rate makes the business an attractive suitable for dividend earnings and dividend development financiers that are searching for methods to produce additional earnings in the type of Dividends.

I think that the BHP Group is presently relatively valued, which is based upon the business’s P/E [FWD] Ratio presently being 13.86. The business’s Typical P/E [FWD] Ratio over the previous 5 years stands at 13.22, validating my financial investment thesis that the business is presently relatively valued.

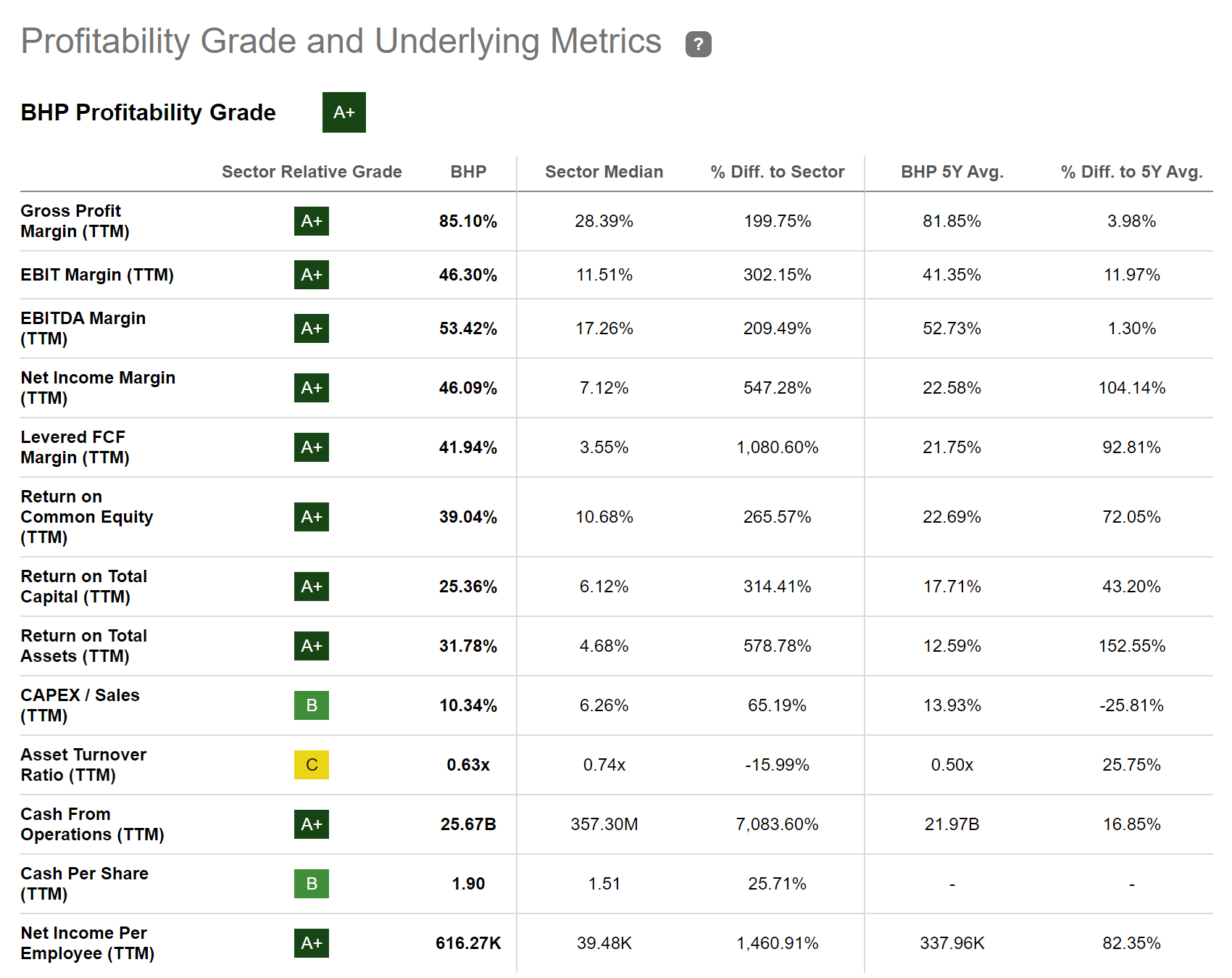

In addition to that, I want to highlight that the business is an exceptional choice when it concerns Success. This thesis is validated by taking a look at the business’s EBIT Margin [TTM] of 46.30% (the EBIT Margin [TTM] of the Sector Mean is 11.51%) and its Return on Equity of 39.04% (the Return on Equity of the Sector Mean is 10.68%).

The Looking For Alpha Success Grade highlights the business’s strength in regards to Success.

Source: Looking For Alpha

Energy Transfer

At the business’s present cost level of $12.74, the business pays a Dividend Yield [FWD] of 9.73%. In addition to that, it deserves pointing out that the business’s ten years Dividend Development Rate [CAGR] stands at 5.76%, suggesting that financiers must not just take advantage of an appealing Dividend Yield, however likewise from the reality that the business’s Dividend might continue to grow within the upcoming years.

Nevertheless, it needs to be discussed that I do rule out the business’s Dividend to be completely safe. The factor for that is that its Payment Ratio lies at 82.65%. This fairly high Payment Ratio adds to the reality that I recommend underweighting the business in a financial investment portfolio, assisting you minimize the drawback danger of your portfolio.

Nonetheless, I think that Energy Transfer is presently an appealing suitable for financiers when thinking about danger and benefit, which can be shown by the business’s Free Capital Yield [TTM] of 15.69%. This number can be utilized as a clear indication that financiers can take advantage of a financial investment without depending on the business conference high development expectations.

In addition to the above, I want to highlight that I think the business is presently relatively valued. This presumption is based upon the reality that the business’s P/E Non-GAAP [FWD] Ratio lies at 9.07, which is 1.17% above the Sector Mean and just 9.31% above the business’s Typical P/E [FWD] Ratio over the previous 5 years.

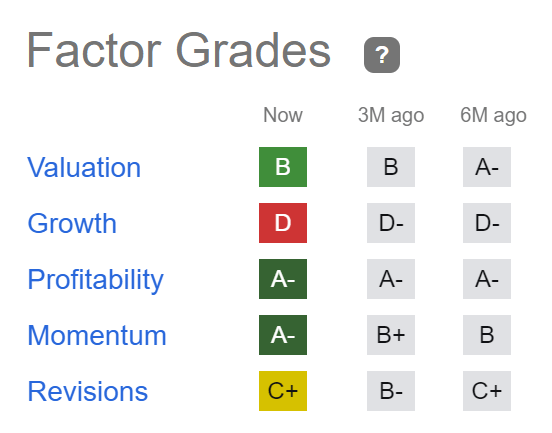

The Looking For Alpha Aspect Grades even more reinforce my belief that the business is presently a fantastic choice for financiers: it is ranked with an A- in regards to Success and Momentum, with a B for Assessment, and with a C+ for Modifications.

Source: Looking For Alpha

Rio Tinto

Rio Tinto was established in 1873 and presently has a Market Capitalization of $108.81 B. The business supplies financiers with a Dividend Yield [FWD] of 6.93%.

At the business’s present cost level, it has a Totally Free Capital Yield [TTM] of 9.09%, which suggests that the business is an exceptional option in regards to danger and benefit at this minute of composing.

Over the previous years, the business has actually likewise revealed exceptional outcomes when it concerns Dividend Development: the business’s Dividend Development Rate [CAGR] over the previous ten years stands at 11.51%, which lies 94.30% above the Sector Mean.

The business’s present P/E [FWD] Ratio of 7.31 more suggests that the business is presently underestimated given that it lies 45.54% listed below the Sector Mean (13.43 ).

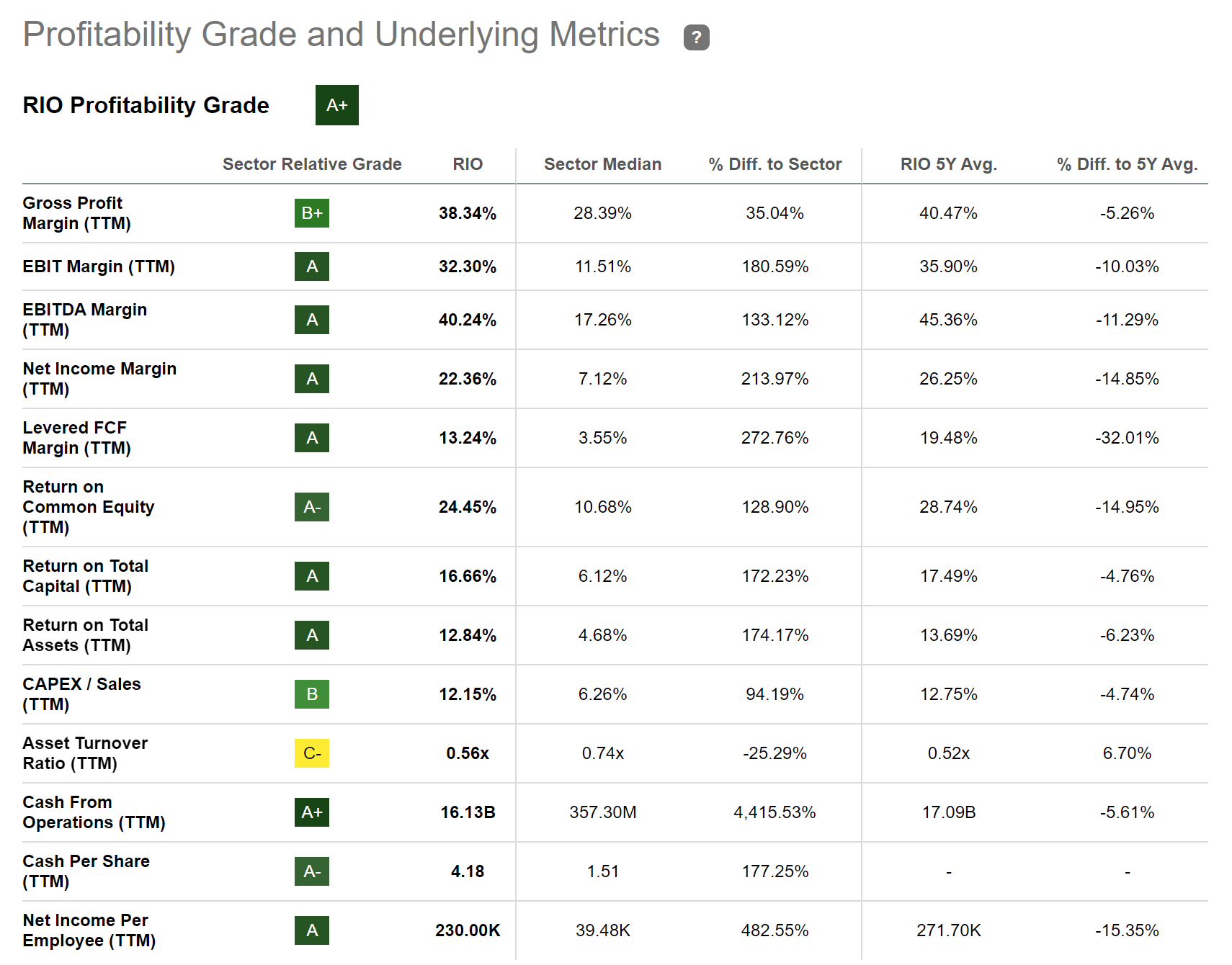

The Looking For Alpha Success Grade reveals us that Rio Tinto deals with a strong Success: the business’s EBITDA Margin [TTM] stands at 40.24% and its Return on Equity is 24.45%, both underlying the business’s strength in regards to Success.

Source: Looking For Alpha

Société Générale

Société Générale supplies banking and monetary services and it runs through the following sectors:

- French Retail Banking

- International Retail Banking & & Financial Providers

- Worldwide Banking and Financier Solutions

The French bank was established back in 1864. It presently has 117,000 staff members.

At the business’s present stock cost of $5.10, it pays investors a Dividend Yield [FWD] of 7.13%.

In my viewpoint, the French bank is presently underestimated. This is validated when taking a look at the business’s present P/E [FWD] Ratio of 6.02, which lies 33.54% listed below the Sector Mean of 9.06. These metrics reinforce my self-confidence to think that the bank is underestimated at its present cost level.

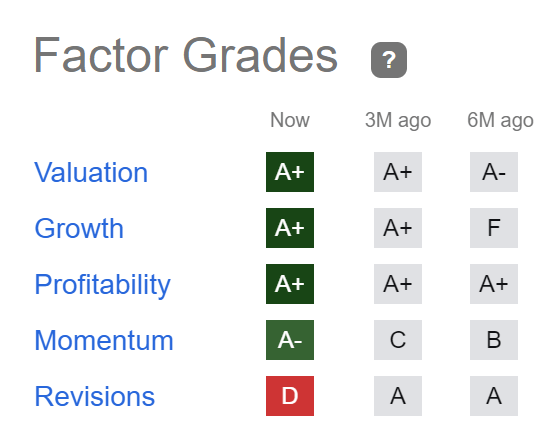

The Looking For Alpha Aspect Grades likewise show that the business might result to be an exceptional financial investment. The French bank is ranked with an A+ in regards to Assessment, Development, and Success. For Momentum, it gets an A-, and for Modifications, a D.

Source: Looking For Alpha

Nevertheless, I do rule out the French banks dividend to be safe (which is more highlighted by Looking for Alpha’s D Score in regards to Dividend Security). For that reason, I recommend to just underweight the French bank in a financial investment portfolio in case you choose to include it into your portfolio. I even more advise offering the bank an optimum of 2% of your total financial investment portfolio with the goal of minimizing the danger level for your financial investment portfolio and herewith to increase the likelihood of getting exceptional returns over the long term.

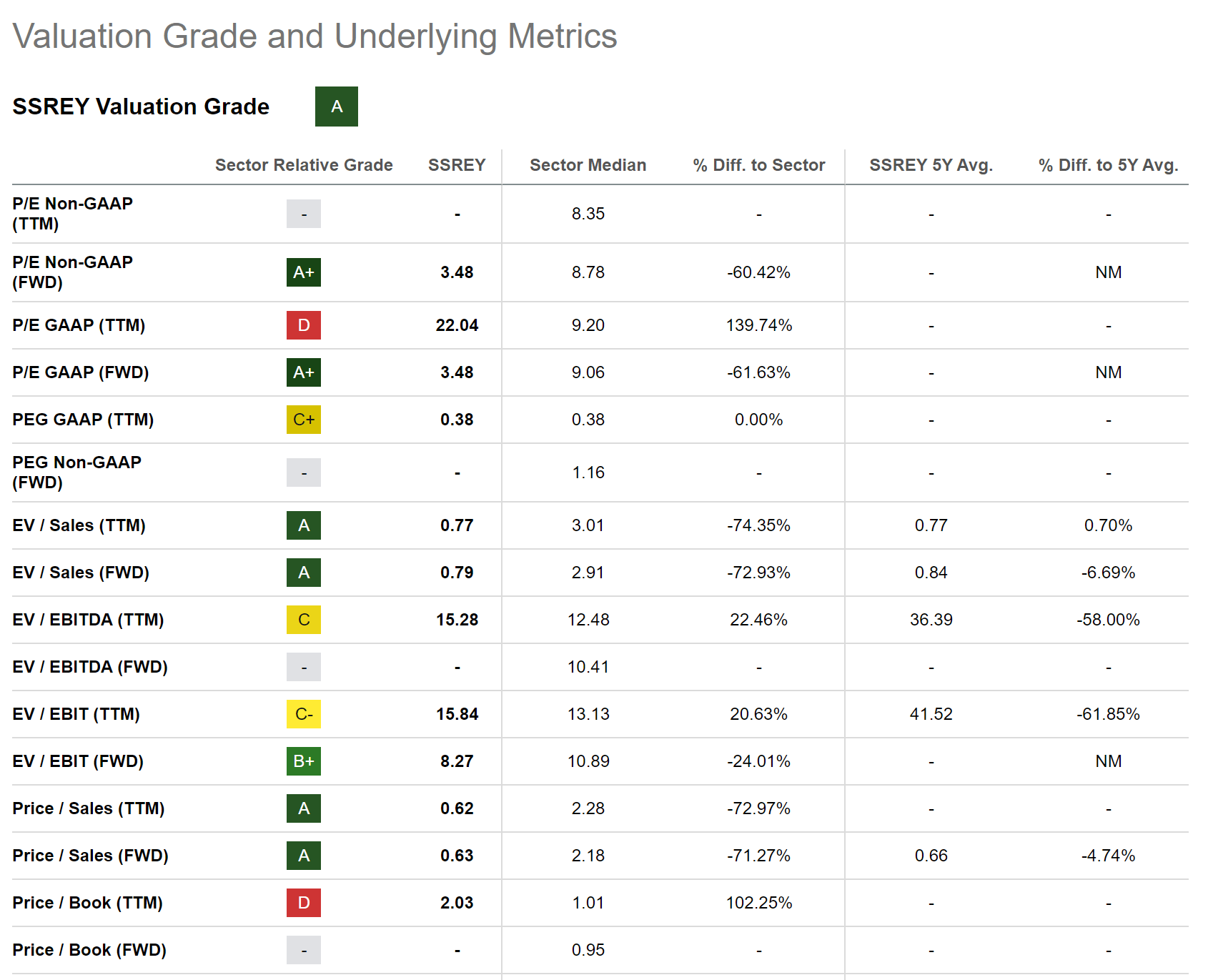

Swiss RE

Swiss RE supplies reinsurance and insurance coverage services worldwide. The business runs through the following sectors:

- Residential Or Commercial Property & & Casualty Reinsurance

- Life & & Health Reinsurance

- Business Solutions

The business presently pays a Dividend Yield [FWD] of 6.54%. It has actually even more revealed a Dividend Development Rate [CAGR] of 4.64% over the previous 5 years. These numbers have actually added to the reality that I think it might be a fantastic choice for those financiers that want to integrate a high Dividend Yield with Dividend Development.

In regards to Assessment, I want to highlight that Swiss RE presently has a P/E GAAP [FWD] Ratio of 3.48, which lies plainly listed below the Sector Mean of 9.06, suggesting that the business is underestimated at its present cost level.

Listed below you can discover the Looking for Alpha Assessment Grade, which highlights the business’s beauty when it concerns Assessment and can be viewed as extra proof that Swiss RE is presently underestimated.

Source: Looking For Alpha

The business even more appears to be an appealing fit when it concerns Development, which is highlighted by its EBIT Development [YoY] of 43.04%, which is plainly above the Sector Mean of 5.11%, and its EPS Diluted Development [YoY] of 58.27%, that is likewise substantially above the Sector Mean (-2.36%).

Altria

Within the previous 5 years, Altria has actually revealed an efficiency of -22.33%. This unfavorable efficiency has actually added to the reality that the business has an appealing stock cost today. At the business’s present cost level of $44.50, Altria has a P/E [FWD] Ratio of 9.41.

The business’s present Assessment lies 26.51% listed below its Typical over the previous 5 years, plainly suggesting that Altria is presently underestimated. This is likewise validated when taking a look at the business’s Dividend Yield [TTM] of 8.45%, which lies 17.39% above its Typical from over the previous 5 years.

Altria pays investors a Dividend Yield [FWD] of 8.45% and has a Payment Ratio of 75.92%. I translate the business’s Payment Ratio of 75.92% in a manner that its Dividend is not completely safe. For this factor, I recommend that you restrict the percentage of the Altria position to an optimum of 5% of your overall financial investment portfolio when choosing to consist of the business in your portfolio.

When compared to Philip Morris (NYSE: PM), I think that Altria is somewhat exceptional when it concerns Dividend Yield (Altria’s Dividend Yield [FWD] is 8.45% while Philip Morris’ is 5.28%), Dividend Development (Altria’s 5 Year Dividend Development Rate [CAGR] is 6.69% while Philip Morris’ is 3.15%) and in regards to Success (while Altria’s Gross Revenue Margin is 68.82%, Philip Morris’ is 63.58%).

I likewise think that Altria is more appealing than Philip Morris in regards to Assessment, which is validated by the business’s lower P/E [FWD] Ratio of 9.41 when compared to Philip Morris’s (P/E [FWD] Ratio of 15.74).

AT&T

AT&T has a variety of competitive benefits, supplying the business with a financial moat over brand-new business that might participate in its organization section: amongst the business’s competitive benefits are its strong brand name image (according to Brand Name Financing, AT&T is presently 22 nd in the list of the most important brand names worldwide), its broad consumer base, the business’s economies of scale and its network facilities.

At this minute of composing, I think that the business has an appealing Assessment: AT&T presently has a P/E [FWD] Ratio of 6.82. This suggests that the business’s P/E [FWD] Ratio presently lies 40.34% listed below its Typical over the previous 5 years. It likewise lies 61.71% listed below the Sector Mean. For that reason, I think that AT&T is presently underestimated.

Listed below you can discover the Looking for Alpha Assessment Grade which raises my self-confidence that the business is an appealing choice in regards to Assessment at this minute in time.

Source: Looking For Alpha

AT&T presently pays a Dividend Yield [FWD] of 7.03%, which reveals that the business is especially appealing for dividend earnings financiers that intend to develop additional earnings in the type of Dividends.

Nevertheless, it holds true that the business has actually restricted development point of views (the business’s Average Earnings Development Rate [YoY] over the previous 5 years stands at 0.22%), and for this factor I recommend underweighting AT&T in your financial investment portfolio. This assists you reduce the danger level of your portfolio while increasing the likelihood of attaining exceptional financial investment results over the long term.

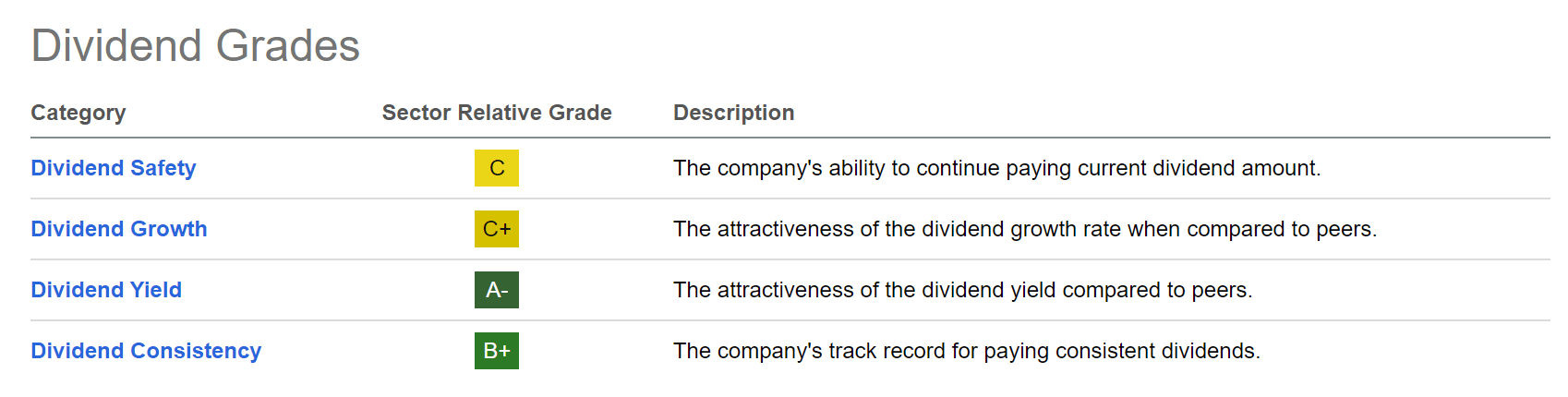

The Bank of Nova Scotia

Over the previous 12-month-period, The Bank of Nova Scotia has actually revealed an Overall Return of -18.02%, which has actually led to the bank presently having a P/E [FWD] Ratio of 9.53. Its present P/E [FWD] Ratio lies 5.89% listed below the bank’s Typical over the previous 5 years, suggesting that the bank is underestimated at this minute of composing.

At the bank’s present stock cost of $48.78, the Canadian bank pays its investors a Dividend Yield [FWD] of 6.37%. In addition to this appealing Dividend Yield, it deserves pointing out that the bank has actually revealed a Dividend Development Rate [CAGR] of 4.74% over the previous 3 years, making me think that it is among these business that can supply financiers with an appealing mix in between dividend earnings and dividend development.

Moreover, it is notable to highlight that the bank has actually currently revealed 17 Successive Years of Dividend Payments, which can be analyzed as an extra indication that reveals that the bank is appealing for dividend earnings financiers.

When compared to U.S. banks such as JPMorgan (NYSE: JPM) or Bank of America (NYSE: BAC), it can be specified that The Bank of Nova Scotia pays a substantially greater Dividend Yield. While the Canadian bank pays investors a Dividend Yield [FWD] of 6.37%, JPMorgan’s Dividend Yield [FWD] presently stands at 2.89%, and Bank of America’s at 3.14%.

Nevertheless, it needs to be highlighted that these U.S. banks have a substantially lower Payment Ratio than their Canadian rival: while JPMorgan’s Payment Ratio lies at 29.52%, Bank of America’s stands at 26.13%; The Bank of Nova Scotia’s Payment Ratio is 52.95%, suggesting that its Dividend is less safe than the Dividend from the U.S. banks which these U.S. banks have more space for future Dividend improvements.

These U.S. banks have actually likewise revealed greater Dividend Development Rates recently: while The Bank of Nova Scotia’s Dividend Development Rate [CAGR] over the previous 5 years is 4.38%, JPMorgan’s is 12.91% and Bank of America’s is 12.89%, suggesting that they might be the much better choices in regards to Dividend Development.

In my viewpoint, The Bank of Nova Scotia is likewise a fantastic choice when thinking about Success: the bank has an Earnings Margin of 29.36%, which lies 13.61% above the Sector Mean.

Listed below you can discover the outcomes of the Looking for Alpha Dividend Grades, which when again, validate the bank’s appealing Dividend: The Bank of Nova Scotia gets an A- for Dividend Yield, a B+ for Dividend Consistency, a C+ for Dividend Development, and a C for Dividend Security.

Source: Looking For Alpha

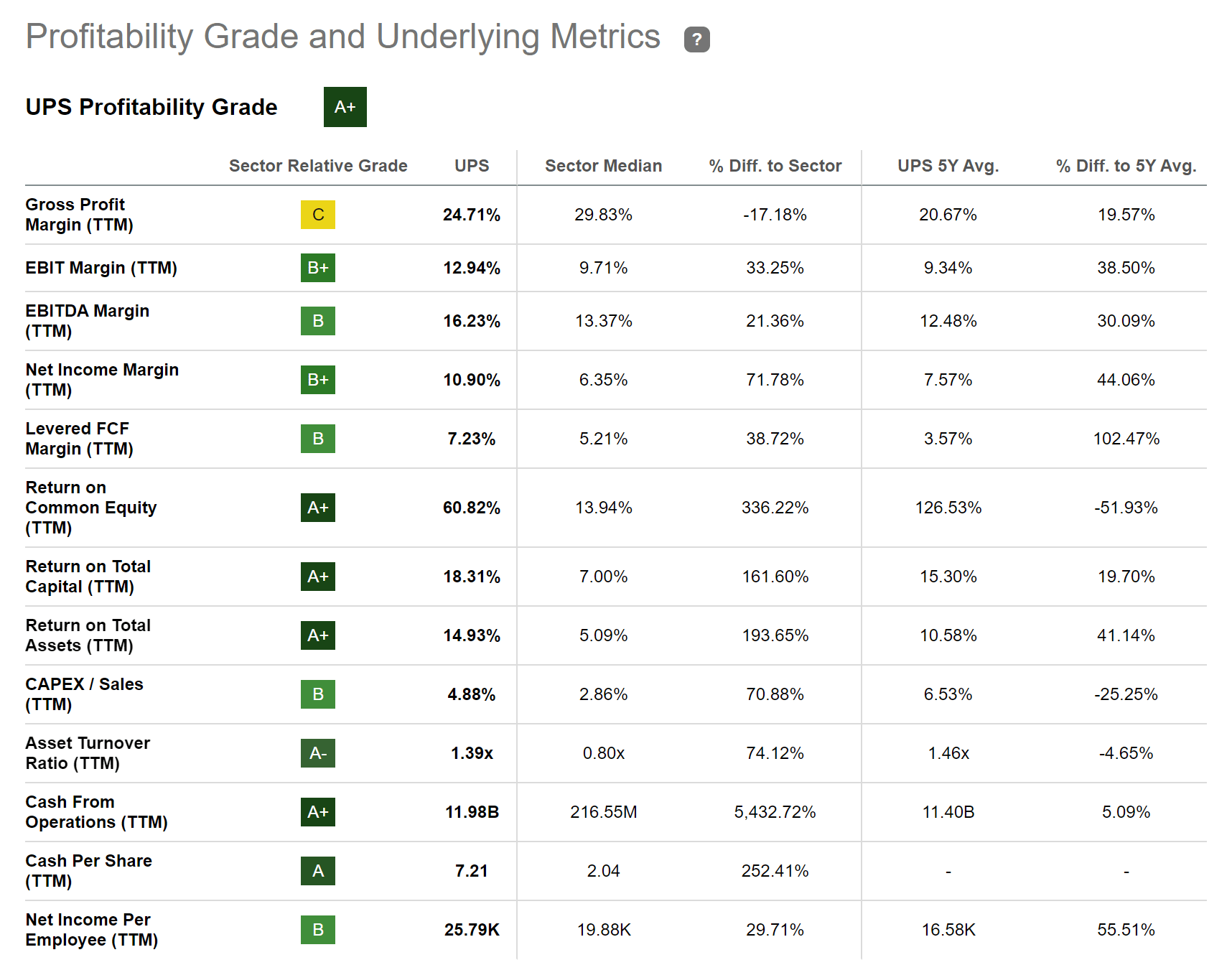

United Parcel Solutions

United Parcel Providers is likewise amongst these kinds of business that integrates a reasonably high Dividend Yield with Dividend Development, making it possible to make an appealing Dividend Yield from today onwards, while having the ability to increase this quantity at an appealing development rate from year to year.

At this minute of composing, UPS pays a Dividend Yield [FWD] of 3.71%. The business’s Payment Ratio lies at 51.07%. In addition, it deserves pointing out that the business’s Dividend Development Rate [CAGR] over the previous 3 years is 16.81%, which is substantially above the Sector Mean of 7.62%. This acts as an extra indication that financiers must not just take advantage of the business’s fairly high Dividend Yield, however likewise from the reality that the business supplies your portfolio with Dividend Development.

I even more think that UPS is at least relatively valued: this is due to the fact that its P/E [FWD] Ratio of 16.33 lies 14.01% listed below the Sector Mean of 19.00. In addition to that, it just stands 1.53% above the business’s Typical P/E [FWD] Ratio over the previous 5 years, validating its reasonable Assessment.

It deserves highlighting that UPS (P/E [FWD] Ratio of 16.33) has a somewhat greater Assessment when compared to FedEx (NYSE: FDX) (P/E [FWD] Ratio of 14.73), however its Assessment is substantially lower than the Assessment of Amazon (NASDAQ: AMZN) (82.56) (due to the reality that Amazon broadens increasingly more its logistics abilities, they can be thought about rivals in particular companies). Nevertheless, I see UPS as the most appealing choice for dividend earnings financiers, which is based upon the reality that it pays a Dividend Yield [FWD] of 3.71% while FedEx’s is 2.03% (Amazon does not pay a Dividend). Nevertheless, I see FedEx somewhat ahead of UPS when it concerns Dividend Development: FedEx’s Dividend Development Rate [CAGR] over the previous 5 years is 23.99%, while UPS’ is 12.53%.

The Looking For Alpha Success Grade even more reinforces my belief that the business has strong monetary health: UPS has an EBIT Margin [TTM] of 12.94% and a Return on Equity [TTM] of 60.82%.

Source: Looking For Alpha

Verizon

Verizon was established in 1983 and I likewise think it has strong competitive benefits that avoid other business from entering its organization section: to call simply a few of them, Verizon has a strong brand name credibility (it is ranked 8 th in the list of the most important brand names worldwide according to Brand Name Financing), a strong network (due to its cordless and fiber-optic networks) and a broad consumer base along with a concentrate on development (which is likewise revealed by its 5G networks).

At today’s stock cost of $36.72, Verizon pays its investors a Dividend Yield [FWD] of 7.09%, acting as a sign that the business is appealing for dividend earnings financiers. It is more worth pointing out that Verizon has actually revealed a Dividend Development Rate [CAGR] of 2.42% over the previous ten years, which shows that financiers must have the ability to increase their extra earnings in the type of dividends yearly when purchasing Verizon.

I consider this mix of Dividend Earnings and Dividend Development really essential for financiers, given that it assists financiers end up being significantly secured from stock exchange cost variations.

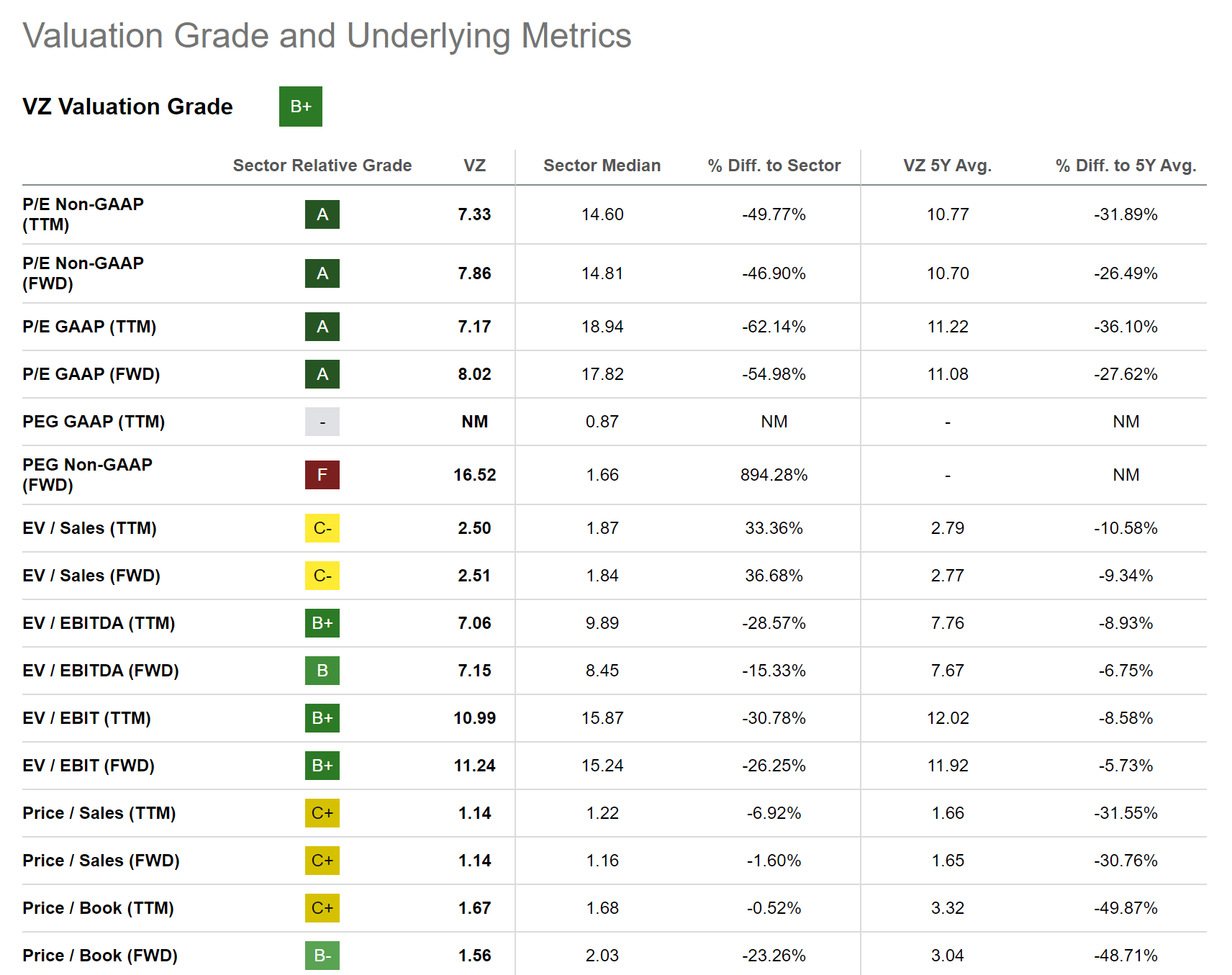

I even more think that Verizon is underestimated. My viewpoint is based upon the reality that Verizon’s P/E [FWD] Ratio of 8.02 stands 54.98% listed below the Sector Mean. It can likewise be highlighted that it lies 27.62% listed below its Typical over the previous 5 years.

Listed below you can discover the Looking for Alpha Assessment Grade, which highlights my theory that Verizon is presently underestimated.

Source: Looking For Alpha

Conclusion

Carrying out a financial investment method that intends to integrate Dividend Earnings with Dividend Development assists you end up being less impacted by stock exchange cost variations.

The focus of this post was on business that especially supply your financial investment portfolio with an appealing Dividend Yield, assisting you increase the Weighted Average Dividend Yield of your portfolio.

I think about these choices to presently be appealing in regards to Assessment, which is shown by the reality that 8 out of the 10 chosen business presently have a P/E [FWD] Ratio listed below 10. In addition, they have strong competitive benefits and are economically healthy, raising my self-confidence that they can be appealing long-lasting financial investments.

With my financial investment analyses, I intend to assist you develop a varied long-lasting financial investment portfolio with a lowered danger level that assists you produce additional earnings in the type of Dividends (integrating Dividend Earnings with Dividend Development) while focusing on the pursuit of Overall Return, including both Capital Gains and Dividends.

Author’s Note: I would like to hear your viewpoint on my choice of high dividend yield business to purchase in July 2023. Do you currently own or prepare to obtain any of the choices? Which are presently your preferred high dividend yield business? If you want to get an alert when I release my next analysis, you can click the ‘Follow’ button.

Editor’s Note: This post goes over several securities that do not trade on a significant U.S. exchange. Please know the threats connected with these stocks.